Structured settlements offer many benefits compared to a lump sum settlement. One of the most important advantages is the option of receiving lifetime benefits. With lifetime structured settlement payments, unlike a lump sum settlement, it is impossible to outlive your settlement award.

This priority for long term security is exactly what led to the creation of multiple laws and regulations aimed at providing important public benefits to structured settlements. As stated by Senator Max Baucus in 1998:

“[O]ur focus in enacting these tax rules in sections 104(a)(2) and 130 of the Internal Revenue Code was to encourage and govern the use of structured settlements in order to provide long-term financial security to seriously-injured victims and their families and to insulate them from pressures to squander their awards.” Public policy has similarly influenced state legislators and various regulators to favor structured settlements.

Unfortunately reports from experienced plaintiff attorneys suggest that lump sum awards are often completely gone in a few short years after they are received. Most settlement recipients have likely never had to think about managing a large sum of money, especially not money that is intended to provide necessary medical care for the rest of their life. This is why it is very important to understand the risks you may face in attempting to manage a lump sum settlement vs. the lifetime protection from a structured settlement.

Mortality Risk

The uncertainty arising from a person’s life expectancy is referred to as mortality risk. Mortality risk can be transferred to a life insurance company when you choose a structured settlement with lifetime payments. Most often, lifetime structured settlement payments are also combined with a “period certain.” For example, you may hear the term, “Life or 30 years period certain.” In this event, the structured settlement payments are made for as long as you live or for the period certain, whichever is longer. If an individual dies during the period certain, all remaining payments are made to a pre-designated beneficiary.

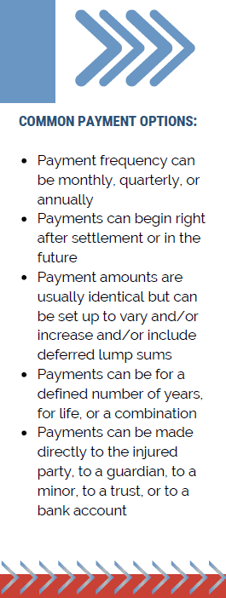

Structured settlement benefits are extremely flexible. So, in addition to lifetime payments and period certain payments, other features are also available.

For examples: structured settlement payments can begin immediately following settlement or the payment start date can be deferred; payments can include deferred lump sums; payments can increase annually.

Reinvestment Risk

When you accept a lump sum, and attempt to invest that money to plan for your lifetime expenses, you also assume a second risk called a “reinvestment risk.” While you may be able to fund your future obligations by investing today at a known rate of return over a known time period, it is not certain or guaranteed what yield will be available for reinvestment at a later time. This uncertainty is known as reinvestment risk. Reinvestment risk (like mortality risk) can be transferred to a life insurance company with a structured settlement that provides benefits for the life of an individual, including an optional period certain.

Structured Settlement Pricing

The pricing of a structured settlement with lifetime payments can involve multiple factors. To enhance security, most structured settlement cases are funded using assignment companies which are generally affiliates of the life companies that issue the structure settlement annuities. Each annuity issuer publishes its own rate sheets, showing the cost of various types of annuities based on a person’s age and sex. The term “standard age rating” implies that, for purposes of annuity pricing, the recipient is considered to have a normal life expectancy. Rates vary at any given time among annuity issuers and also vary with changes in market interest rates.

When medical conditions suggest an individual’s life expectancy is less than normal, it is common for a life insurer to conduct a medical and actuarial analysis to assign what is referred to as a “rated age.” This rated age is important because it will often result in greater monthly benefits for lifetime payments regardless of how long the person lives. Future changes in their medical condition will not impact the life insurer’s original assessment or payment amounts.

Structured Settlement Consultants

Structured settlement consultants play important roles in the process of identifying settlement recipients who have the potential for receiving rated ages and also for obtaining and submitting the medical information required by the life company’s medical actuaries who determine the rated age that can increase the amounts of monthly structured settlement payments a claimant receives. They can also help you match structured settlement features to your specific needs and objectives.

For all of these reasons, the only way you can safely protect your settlement for life is to choose a structured settlement.