Introduction

Nearly fifty years have passed since the first structured settlement studies sought to measure how periodic payments could reshape personal injury compensation. In that half-century, the industry has evolved from a defense-side experiment in claims management into a broader settlement planning profession, one that integrates claimant financial security with tax efficiency, government benefits protection, and long-term income management. Through all those years, various surveys provide an insightful lens into the threads that connect the stages of industry development.

From the 1977 Lilly Study to MetLife’s 2025 Claimant Survey, research has served as the industry’s mirror and its map: reflecting how structured settlements were understood in their time and revealing where they might go next. Across five decades, these surveys document the industry’s transformation, its expanding participants, its evolving priorities, and the gradual shift from measuring cost control to measuring client outcomes.

This article, the first in a three-part series, begins by tracing that history. Part One reviews the major surveys that shaped structured settlement understanding from the 1970s through the 2020s, showing how each reflected the perspectives of its era, insurers, regulators, brokers, consultants, plaintiff attorneys, and finally claimants themselves. Part Two will analyze what those surveys reveal about today’s challenges and the opportunities they create for growth and modernization. Part Three will look ahead, translating the new evidence of claimant outcomes into professional standards and measurable practice.

Together, the three parts aim to do more than summarize five decades of research. They offer a continuous narrative, a record of how structured settlements evolved from an idea into an established industry; how, informed by data and experience, the industry is fully maturing into a comprehensive settlement-planning profession defined by evidence, education, and enduring public value; and, the keys to unlock the industry’s yet-remaining substantial growth potential.

The Origins and Early Evolution of Structured Settlement Research.

Structured settlements in the United States find their origins in the mid-1970s, when domestic insurance pioneers first began structuring legal settlements in the form of periodic payments. These early structuring activities served as the catalyst for the enactment, years later, of the Periodic Payment Settlement Act of 1982, the formative legislation that cemented the legal and tax foundation of structured settlements and spurred the growth of an entire industry over the next five decades.

Coincidentally, the TV show Family Feud also debuted in the mid-1970s, coining the phrase “And the Survey Says!” That popular phrase is apropos to this article because key industry participants conducted and published numerous surveys over the last 50 years in an effort to compile valuable data on structured settlements, and these “surveys say” a lot about structured settlements, providing both snapshots that reflect the state of the industry at the time they were produced as well as, in many ways, a moving motion picture of the industry’s evolutionary path over time.

Understanding who conducted these surveys and what they measured isn’t merely an academic exercise, it offers today’s consultants and carriers (both casualty and life) a lens through which to see how the industry’s priorities shifted over time and where their own role now fits within that evolution.

In the earliest years, structured settlement research was sponsored mainly by property-casualty insurers and regulatory or governmental bodies focused on claims management outcomes. As the market matured, industry associations such as the National Structured Settlements Trade Association (NSSTA) and, later, the life insurers funding structured-settlement annuities assumed that role. The respondent base likewise broadened, from defense-side insurers and claims managers to settlement consultants, plaintiff attorneys, and eventually claimants themselves.

Each generation of surveys reflected its sponsors’ objectives: early studies measured claims efficiency and cost control; later surveys examined education, satisfaction, and financial outcomes. Viewed together, these studies trace the industry’s gradual expansion from a narrow, insurer-driven experiment in claims management to a multidisciplinary system connecting insurance, law, and long-term settlement planning.

The bookends of these surveys and studies evaluated in this article are, on the one hand, the narrowly focused, claims-oriented 1977 Lilly Survey produced at the genesis of the industry and, at the other end of the spectrum both in time and scope, the broadly expanded, plaintiff-focused 2025 MetLife Survey. Together, these studies define the scope of inquiry for this article, examining five decades of data to understand how structured-settlement research evolved, what it reveals about the profession today, and what questions remain for Parts Two and Three of this series to address.

Key Surveys and Studies Since Industry Inception.

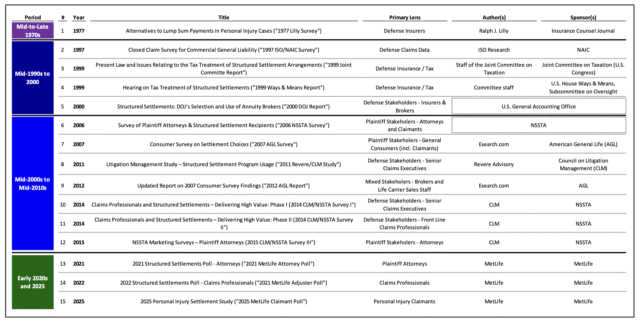

Before this article turns to discussing highlights of most of the surveys and studies, here is a list of the 15 surveys, studies and reports (collectively referred to as “surveys”) discussed throughout this article.

1970s: Defense Origins and the First Structured Settlement Survey.

Widely regarded as the first empirical look at structured settlements, the 1977 Lilly Survey asked 82 casualty insurers whether they had used periodic payments, attempted them unsuccessfully, or relied solely on lump-sum policies. Although the survey mentioned claimant advantages as policy justifications, its focus was operational – examining claims reserving, indemnity costs, and carrier procedures to determine whether periodic payments could improve efficiency and reduce overall payouts. In other words, the survey tested the product’s value as a claims-management experiment rather than as a financial-planning tool for injured people. This early study was therefore a supply-side proof of concept, driven by defense insurers exploring cost control and risk management. Claimant-focused considerations would not meaningfully appear in survey data for nearly thirty years—until, starting in 2006, studies finally began to ask how structured settlements affected the people who actually received them.

1990s to Early-2000s: The Mature Defense Era.

Four (4) key structured settlement surveys, studies and reports were conducted during this period that, like the 1977 Lilly Survey, continued to reflect a defense-side, claims management orientation. Unlike the Lilly Survey, however, these surveys were commissioned by self-regulatory and government bodies.

The most relevant of these surveys to this article was the 1997 ISO/NAIC Survey. Compared with its Lilly predecessor, this 1997 survey substantially expanded the quality of claims data available to the industry and reflected the next phase of industry evolution. In the late 1970s, structured settlements were a nascent innovation championed by defense insurers seeking cost control and efficiency. By the 1990s, structured settlements were an established practice for resolving large-injury claims, integrated into mainstream defense insurer settlement strategies. Unlike its Lilly predecessor, the 1997 ISO/NAIC Survey made no mention of claimant-oriented policy rationales. This study highlights the continued absence of claimant-level focus and research at that time, an informational, philosophical and strategic gap that would not begin to close until yet another decade later.

2006 to 2015: The Shift to Plaintiff and Consumer Perspectives.

By the mid-2000s, the research focus had begun to expand beyond defense priorities. New surveys introduced the voices of plaintiff attorneys and claimants, marking the industry’s transition toward a more balanced, outcome-oriented understanding of structured settlements. From roughly 2006 through 2015, structured settlement survey research entered its most active decade since the industry’s creation. During this period, seven (7) major surveys and reports were produced, reflecting a decisive shift in perspective: for the first time, a majority of studies focused on plaintiff stakeholders and end-users rather than insurers and claims managers.

This shift represented an historic turning point. After nearly thirty years of viewing structured settlements primarily through the lens of defense efficiency, the industry began listening to the people who actually recommend and receive the payments, plaintiff attorneys and claimants. Their responses introduced behavioral and motivational data into what had previously been a claims-management conversation, linking structured-settlement use to human factors such as trust, timing, education, and satisfaction. For today’s structured settlement consultants, this era arguably represents the origin of modern settlement planning: when structured settlements began to be studied not just as financial products, but as experiences shaped by communication, advice, and client understanding.

2006 and 2007: First Plaintiff Attorney and Claimant Studies.

The 2006 NSSTA Survey marked a turning point in structured settlement research. For the first time, it systematically captured voices from both sides of the plaintiff experience: attorneys, the gatekeepers to the use of structured settlements by claimants as well as actual end users themselves via annuity-funded structured attorney fee deferrals, and claimants, the primary consumers of structured settlements. Departing from earlier insurer-driven, supply-side studies, NSSTA focused squarely on the demand-side, gathering direct insight, for the first time in 30 years since industry formation, into the people who depend on structured payments for long-term financial stability.

This 2006 NSSTA study was the first study to position structured settlements within a broader settlement-planning framework, linking legal, financial, and behavioral considerations. The survey explored what motivates claimants to structure, what barriers prevent them from doing so, and how satisfaction relates to timing, education, and product understanding. Its findings reframed structured settlements as behavior-based financial planning tools rather than actuarial cost-control devices. For consultants today, the 2006 NSSTA Survey stands as the industry’s first empirical reminder that successful outcomes begin with early education, clear communication, and meaningful engagement between attorneys, brokers, and claimants.

The 2007 American General Life (“AGL”) Survey built directly on NSSTA’s pioneering work, extending its focus on claimant attitudes and the influence of advisors at the point of decision. Like the NSSTA project, AGL used a dual-participant model—surveying both individuals with personal experience in structured settlements and members of the general public—to compare how familiarity shapes perceptions. Respondents were asked about their awareness of structured settlements, the features they valued most (tax-free income, guarantees, insurer strength), and the concerns that gave them pause (primarily liquidity and flexibility). The findings closely mirrored NSSTA’s results: most claimants first learned about structured settlements from their attorneys, and satisfaction rose sharply when the concept was introduced early and explained clearly. The study reinforced a central theme that remains relevant today, plaintiff attorneys are the decisive gatekeepers, and the quality and timing of their education efforts often determine whether claimants choose structures at all.

The 2007 AGL Survey also differed from the 2006 NSSTA study in important ways. Instead of focusing on structured settlement participants or plaintiff attorneys, it polled a nationally representative sample of 1,000 adults aged 18 and older. This broadened the research lens beyond the settlement process itself to measure how the general public perceived structured settlements, 80% of its respondents had no prior structured settlement experience at all whereas 20% of its respondents had at least some experience with structured settlement as claimants and/or family members thereof. The AGL Survey measured what these people knew, misunderstood, or had never heard before about structured settlements. The results were telling: awareness was low, even among those who might one day benefit from a structure, but once the concept was explained, respondents viewed it overwhelmingly as a positive and responsible financial option. The study thus revealed a parallel opportunity that still exists today, educating the public and allied professionals remains essential to expanding understanding and use of structured settlements.

In short, the 2006 NSSTA Survey showed how attorney conduct and timing influence whether claimants use structured settlements, while the 2007 AGL Survey revealed when and why people form opinions about them in the first place. Viewed together, they offered the industry its first comprehensive glimpse of the demand-side—real attitudes, awareness levels, and decision drivers from both attorneys and consumers. These insights gave stakeholders an evidence-based foundation for improving education, refining messaging, and expanding structured settlement adoption across the marketplace. They also set the stage for the surveys that followed, which tested whether these new claimant-centered insights could reshape the institutional practices that had long defined the field and accelerate the evolution from a structured settlement marketplace to an integrated settlement planning profession.

2010 to 2015: Balancing Defense and Plaintiff Perspectives.

After the plaintiff-oriented breakthroughs of 2006 and 2007, the next wave of surveys—spanning 2010 through 2015—reflected a mixed return to institutional and defense perspectives. Five notable studies appeared during this period, three revisiting claims-side issues and two continuing the shift toward plaintiff and consumer viewpoints.

2011 Revere/CLM Study. This broad survey of litigation-management executives across 30 service areas confirmed that insurers and defense teams had fully integrated structured settlements into their claims-resolution toolkits. Yet, even from a defense vantage, respondents acknowledged a gap: few metrics existed to measure claimant outcomes or program effectiveness. For today’s professionals, Revere’s findings highlight an enduring need for better analytics linking program performance to claimant well-being.

2012 AGL Report. Published five years after AGL’s original public-opinion survey, this report updated and refined earlier findings with clearer visuals and sharper messaging. Labeled For Producer Use Only, it served as an internal training and sales resource for structured-settlement producers, brokers, and life-carrier sales professionals within AGL’s distribution network—some of which would be considered defense stakeholders, some of which would be considered plaintiff stakeholders and some of which could be considered both. The report distilled consumer insights—attorney disclosure gaps, client fund-depletion risks, and the importance of early counseling—into practical guidance for everyday sales and education. In effect, the 2007 survey generated the data, while the 2012 report translated it into professional practice.

2014–2015 NSSTA/CLM Three-Part Series. Returning to a comprehensive frame, this project surveyed 50 senior claims executives, 103 front-line adjusters, and 130 plaintiff attorneys. The results mapped an institutional evolution from sporadic to strategic use of structures. Defense respondents described more formalized programs and clearer performance standards. Plaintiff attorneys generally supported the idea of structures—viewing them as beneficial for clients—but also flagged obstacles such as concerns over liquidity, timing pressure in settlement deadlines, client resistance to delayed access to funds, and the influence of the factoring industry. Some attorneys also mentioned that they felt obligated (or ethically pressured) to mention structured settlement options to clients when justified by case value. Collectively, these studies documented the industry’s gradual professionalization: structured settlements were no longer experimental but embedded within claims operations, though still constrained by education and perception gaps.

Together, the 2010–2015 surveys bridged the industry’s two perspectives—testing how far claimant-centered insights could reshape institutional habits and how defense analytics could inform better client outcomes. For consultants today, they illustrate that genuine growth depends on integrating both: the discipline of program measurement and the empathy of claimant-focused planning.

2020s: Comprehensive Perspectives and Outcome-Based Evidence.

During the early 2020s, MetLife became the industry’s leading source of structured settlement and settlement planning research, producing three complementary surveys that, taken together, provide the most complete data set in the field to date. Each study examined a different vantage point—attorneys, claims professionals, and claimants—creating a 360-degree view of how structured settlements are understood and used in practice.

2021 MetLife Attorney Poll. Surveying more than 250 personal-injury attorneys, this study explored when and why lawyers recommend structured settlements and what support they want from brokers and carriers. These findings highlight how the boundaries between structured settlements and settlement planning have become increasingly interconnected. It combined quantitative polling with qualitative insights into decision drivers behind lump-sum versus periodic payment choices. Most attorneys viewed structured settlements favorably but cited time pressure, client liquidity demands, and limited educational resources as barriers. The overarching message: earlier collaboration and stronger educational tools could significantly improve client outcomes.

2022 MetLife Adjuster Poll. This follow-up surveyed 50 claims leaders to gauge who introduces structures, how formalized programs are, and what additional training is needed. Adjusters reported high awareness of structured settlement benefits and broad willingness to use them personally, yet called for more consistent company policies, clearer metrics, and standardized education. The findings also revealed that greater support from insurers and brokers to standardize best practices was the main constraint on wider adoption.

2025 MetLife Claimant Poll. Surveying 503 settlement recipients (or guardians), MetLife captured the first robust dataset on claimant outcomes and perceptions. It compared budgeting ease, financial security, and satisfaction between lump-sum and structured-payment recipients. The results were striking: annuity payees reported far greater budgeting confidence and long-term security, while many lump sum recipients expressed first-year spending regrets and said budgeting would be easier with periodic payments.

Taken together, the MetLife trilogy confirmed what decades of professional opinion had only implied: structured settlements—now central to a broader settlement planning process—deliver measurable, long-term financial security for claimants and enjoy broad support among plaintiff attorneys and claims professionals when properly explained and implemented. These studies signal a mature research stage—one that measures success through claimant outcomes rather than industry belief.

The 2025 MetLife Claimant Poll also provided new perspective on a long-standing concern first noted in the 2014–2015 NSSTA/CLM surveys—the downstream impact of the factoring industry. Although most respondents expressed satisfaction with their structured payments, a small but meaningful subset who had sold (“factored”) some or all of their future payments reported subsequent regret and diminished financial stability compared with those who retained their full income streams. These findings transform what earlier attorney surveys identified as a professional concern into outcome-based evidence of real claimant experience. Factoring may satisfy short-term liquidity needs, but it often undermines the very financial security structured settlements are designed to preserve. For today’s settlement planners and insurers, this underscores the continuing importance of education, ethical guidance, and payee protection mechanisms to ensure that structured settlements fulfill their intended purpose—sustained, dependable recovery.

While the MetLife studies confirm the enduring benefits of structured settlements, they also expose the obstacles that still constrain their consistent use. Beyond the behavioral and ethical issues highlighted by factoring, adoption remains uneven, limited less by product design than by process—when and how structures are introduced, who explains them, and how results are measured. These are not failures of principle but of practice: challenges of timing, education, and institutional alignment that continue to shape real-world outcomes. Addressing them will determine how effectively the industry converts decades of positive evidence into broader access and measurable public value. Part Two of this series explores these challenges in depth and considers how modernization—through better data, clearer standards, and stronger collaboration—can expand both the reach and the reliability of structured settlement and settlement planning practice.

Conclusion.

Across five decades of research, the structured settlement story has evolved from a claims-management experiment into a more comprehensive settlement planning profession that integrates financial security, tax strategy, and government benefit protection. Each generation of surveys captured a different perspective, but together they chart a continuous path toward a more balanced, outcome-based understanding of what these arrangements achieve.

The evidence now tells a clear story: structured settlements work best when viewed not merely as products but as planning instruments that improve long-term results for injured individuals and their families. Yet the surveys also reveal unfinished business—persistent challenges of timing, education, and data transparency. These issues, and the opportunities they create for innovation and modernization, are explored in Part Two of this series, which turns from history to application—examining how structured settlement insight can be transformed into professional practice and measurable results.

By Patrick Hindert & George Luecke.